BOI: an evaluation

50 years of BOI, investment remain virtually static. Investment promotion without domestic reform is salesmanship without a product.

Board of Investment (Pakistan) – mandate & functions

The BOI is Pakistan’s principal investment promotion & facilitation agency, under the Prime Minister’s Office. (Wikipedia)

Its functions (via the BOI Act / rules) include:

Promoting both domestic and foreign investment in Pakistan (Invest Pakistan)

Facilitating investors in implementing and operating their projects (coordination, “one-window services”) (Invest Pakistan)

Being associated with government in the formulation of policies that impact investment (Invest Pakistan)

Other investor‐support roles: assisting in land, taxation, visa, utilities, regulatory approvals (as per BOI/ordinance descriptions) (LinkedIn)

Organizationally, BOI has wings like Investment Promotion, Ease-of-Doing-Business / Regulatory Reform, Special Economic Zones (SEZs), facilitation, policy & legal, etc. (Wikipedia)

Hence, BOI is meant to act as a bridge or interface between investors and the state, plus influencing the investment climate (policy, regulatory reforms), rather than executing large-scale industrial projects or line-sector development itself.

Overlaps

To understand whether BOI is redundant or not, we must compare its niche vs. what other ministries/structures do. To understand whether BOI is redundant or not, we must compare its niche vs. what other ministries/structures do. Pakistan’s investment landscape is fragmented across overlapping institutions. The Planning Ministry is supposed to coordinate development and growth but has relegated itself to managing the PSDP and making vague announcements without clarity. The Commerce Ministry handles trade policy and export promotion, occasionally intersecting with investment promotion for export-oriented FDI. The Industry Ministry oversees industrial policy, licensing, and sectoral regulation—areas that overlap with BOI’s facilitation but with direct regulatory powers BOI lacks. Provincial BOIs, such as the Punjab Board of Investment, work locally to attract and facilitate projects but often duplicate federal efforts. Finally, the Special Investment Facilitation Council (SIFC) now dominates the coordination space, effectively superseding BOI’s facilitation mandate due to its political and military backing. The result is a maze of agencies with blurred mandates, competing jurisdictions, and no single accountable authority for investment outcomes.

So in summary: BOI sits in the overlap among trade, industry, investment promotion, and cross-ministry coordination. Its value depends on whether it can outperform or complement these other bodies by being faster, more investor-centric, and less bogged by silos.

Evaluation:

Indicators & red flags

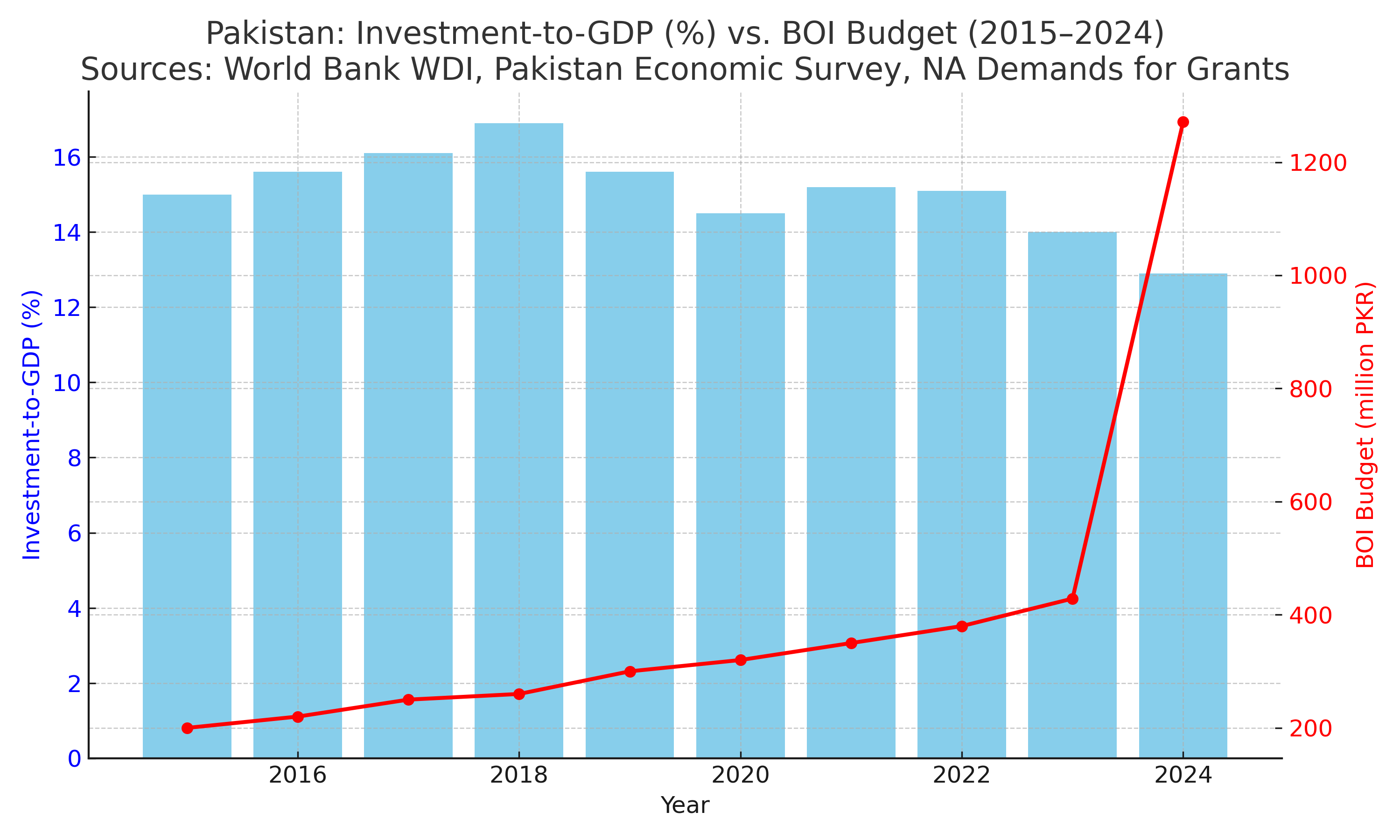

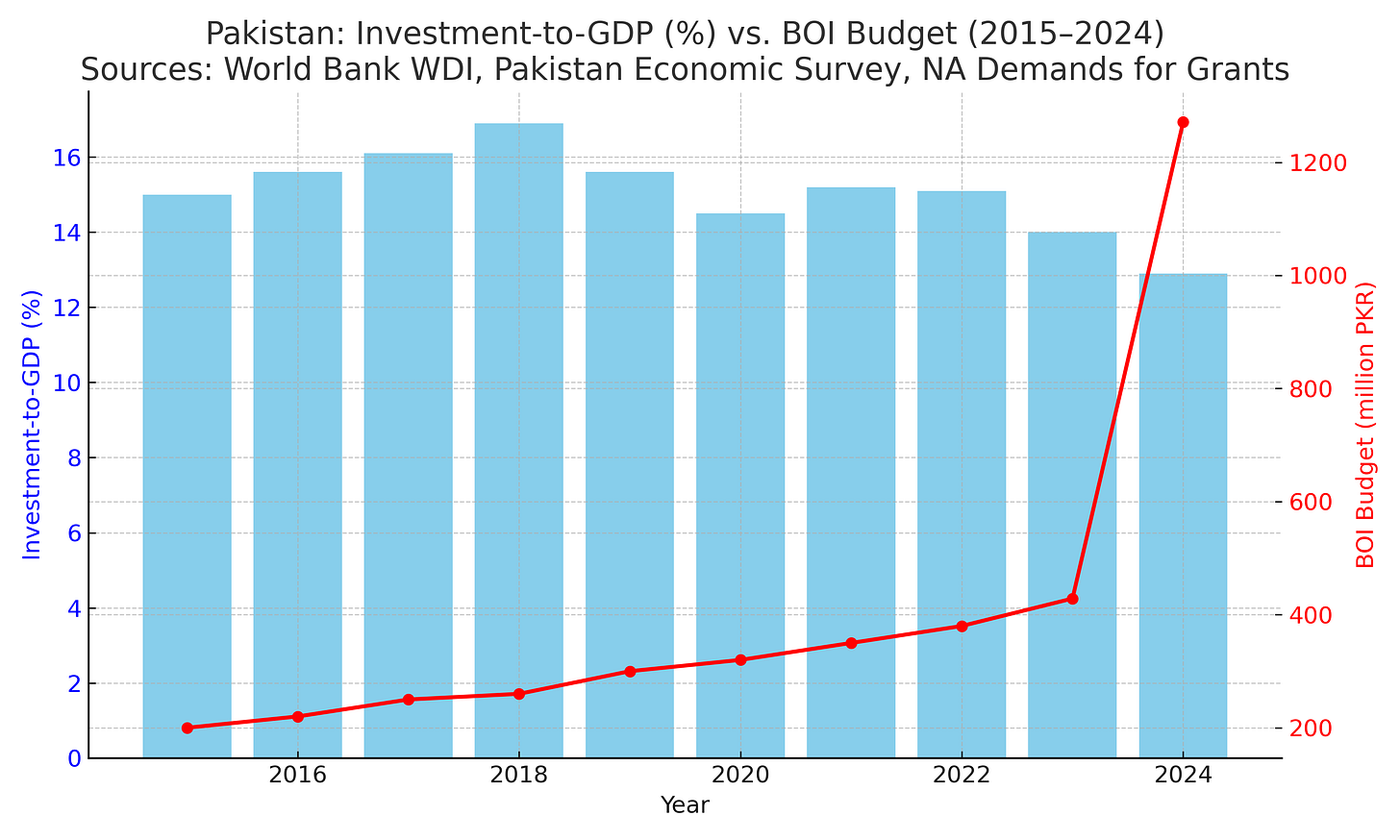

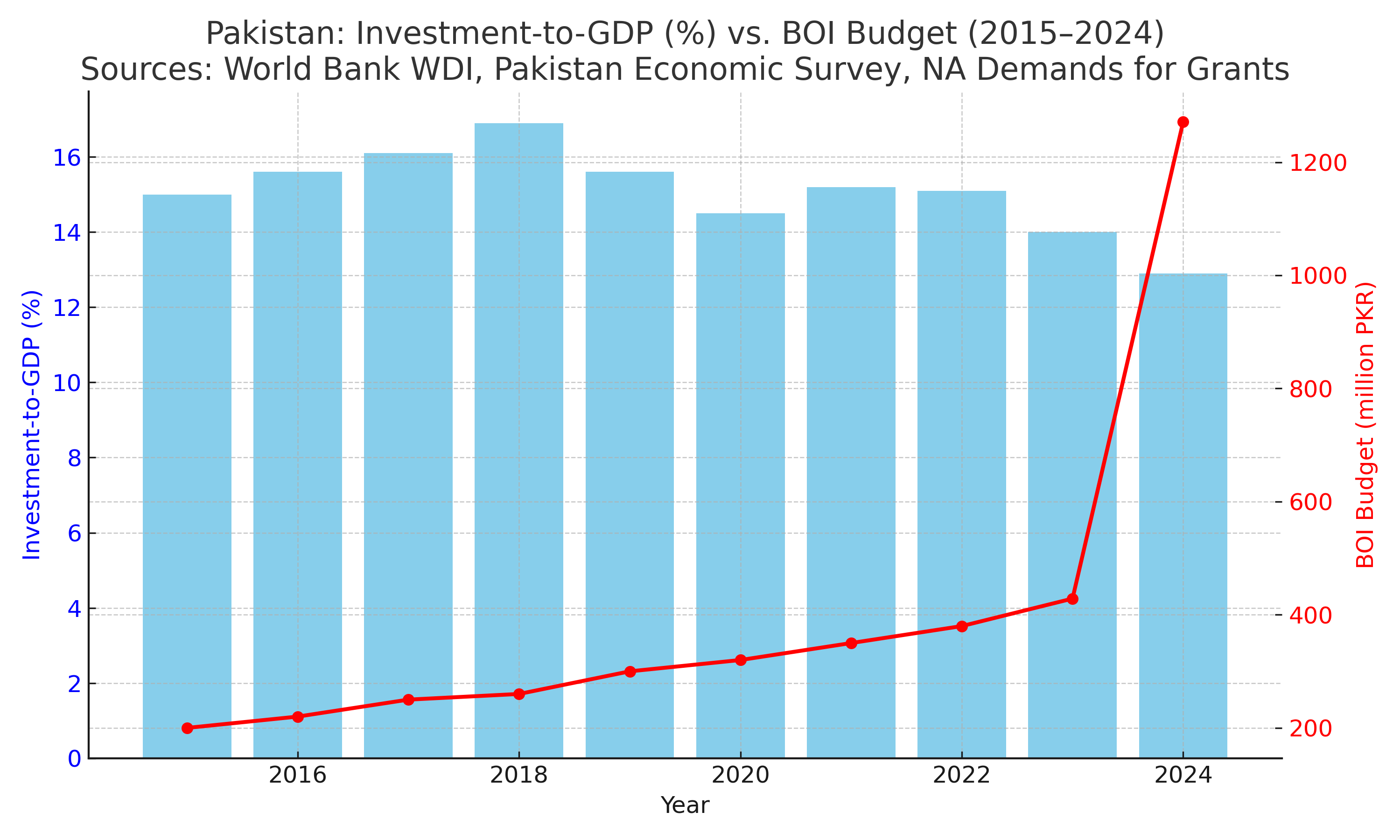

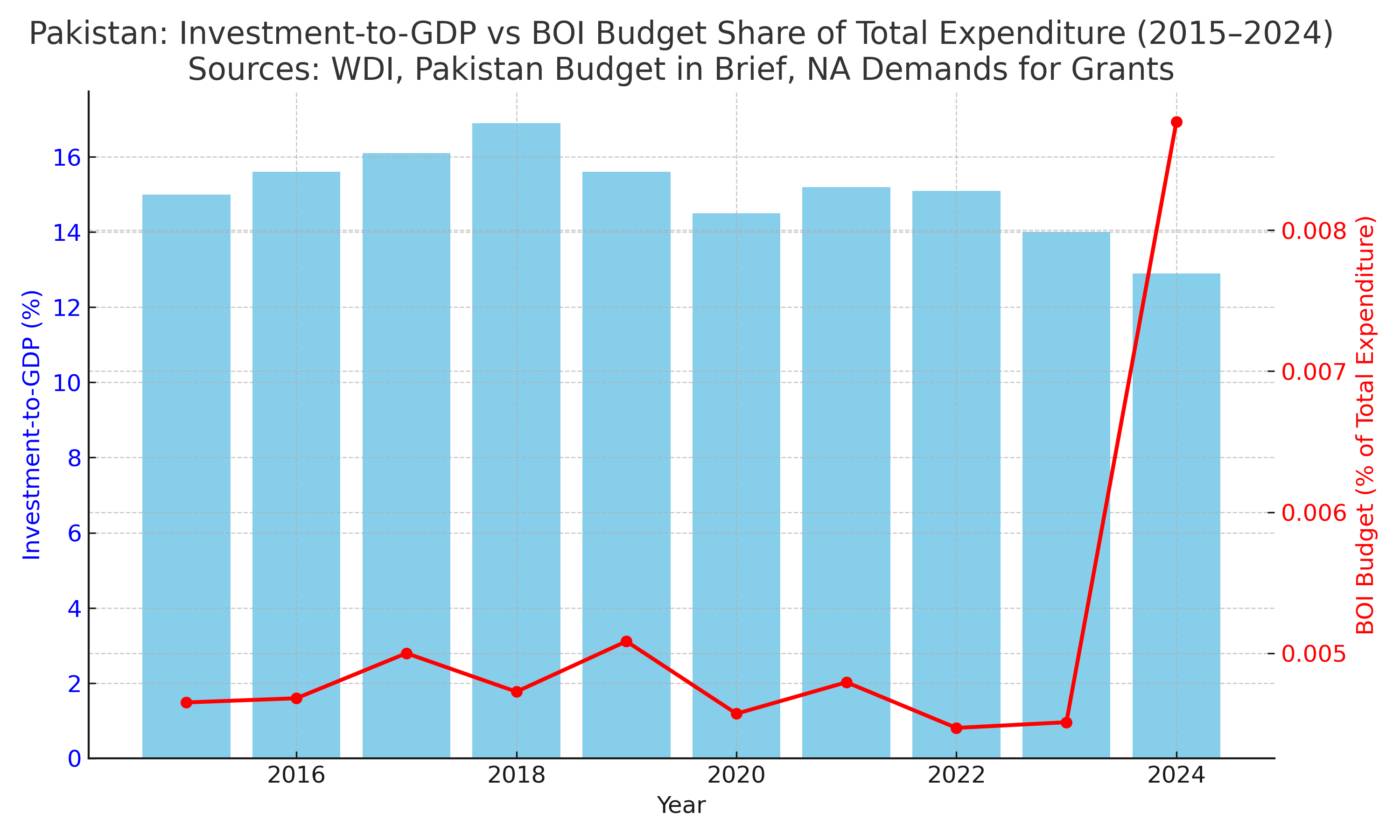

Weak correlation between BOI funding increase and investment growth

You observed that BOI’s budget jumped (e.g. ~3× from FY24 to FY25) but investment-to-GDP (or gross capital formation) is declining or stagnant over the decade. This suggests that increased spending has not yet resulted in visible macro results in investment.

Of course, many intervening variables (macro instability, security, policy consistency, infrastructure bottlenecks) can overshadow BOI’s contribution.

Institutional constraints and capacity

According to the IMF’s Public Investment Management Assessment (PIMA) report, Pakistan still has significant gaps in public investment management (e.g. project selection, monitoring, intergovernmental coordination). (IMF)

BOI is only one part of a much larger system — so even a smoothly running BOI may be stymied by weak infrastructure, legal uncertainty, or regulatory constraints outside its control.

And in real terms

Duplication and weakened comparative advantage

The emergence of SIFC (established in 2023) as a high-powered investment facilitation body risks making BOI redundant (or relegated to a lesser role). (Wikipedia)

Multiple “BOIs” (federal + provincial) create potential for jurisdictional confusion, investor confusion, duplication of outreach, or competition.

Longevity without compelling success

BOI (or its precursors) has existed in some form for decades. Yet, Pakistan’s investment ratio remains low relative to neighbors or benchmarks. If after half a century it has not materially raised or stabilized investment flows, critics would argue the return on institutional existence is weak.

Lack of clear measurable outcomes / rigorous evaluation

Surprisingly there has been no credible, public, independent evaluation of BOI’s performance (e.g. an independent body, or a university or the think tank led) in recent years. That absence is concerning: how do we know whether BOI’s interventions made difference, or whether resources are well spent?

Investment promotion without domestic reform is salesmanship without a product.

For half a century Pakistan’s Board of Investment (BOI) has existed in one form or another — tasked with promoting, encouraging, and facilitating investment. Yet, after five decades of offices, expos, and MoUs, the investment-to-GDP ratio remains stuck near 13%, among the lowest in the region. In FY2024–25, the government tripled BOI’s budget to over Rs 1.2 billion, but the country’s total investment still barely nudged upward. That gap between institutional intent and economic reality captures the story of Pakistan’s “promotion without reform.”

The deeper problem is that foreign investment cannot be divorced from domestic investment. No country has succeeded in attracting sustainable FDI when its own entrepreneurs are retreating. Investors read domestic behavior as the truest signal of a country’s potential. When local businesses are closing plants, shifting wealth to real estate, or moving assets abroad, no global marketing campaign or “ease of doing business” portal can convince foreigners otherwise. Capital follows confidence, and confidence follows predictable rules — not slogans.

Pakistan’s domestic investment climate has collapsed under erratic tax policy and regulatory overload. Every budget rewrites the rules: new levies, arbitrary exemptions, unpredictable withholding taxes, and perpetual disputes over refunds. Businesses are harassed rather than serviced. Add to that over a hundred licensing and inspection regimes — all manual, sequential, and often contradictory — and you get paralysis. The taxman, regulator, and inspectorate have together become the biggest deterrents to productive risk-taking.

That, in turn, exposes a governance vacuum. The ministries that control Pakistan’s investment fundamentals — Finance, Commerce, Industry, Planning, Law, and the provinces — have effectively abdicated. Finance and FBR chase revenue targets, not stability; Commerce clings to protectionism; Industry remains preoccupied with public corporations; Planning which is supposed to coordinate development and growth has relegated itself to PSDP allocations with pronouncements of overambitious targets; and Law has left investors stranded in courts for years. Provincial agencies multiply permissions but not service delivery. The result is a web of uncertainty so thick that even the most determined investor struggles to move from intent to operation.

Pakistan’s investment stagnation is not a mystery — it’s the product of confused mandates, unstable policy, and bureaucratic inertia. BOI’s transformation can only succeed if the rest of the state stops suffocating investors. The day domestic entrepreneurs start building again, foreign investors will line up without a roadshow. Until then, no budget increase or board reshuffle can substitute for credibility.

Nadeem Ul Haque SIA